Overview

Every year, the Parliamentary Budget Office (PBO) prepares a large number of policy costings for parliamentarians. These provide estimates of the impact of the proposed policies on the Australian Government Budget over the next decade.

Individual policies can affect the Budget through a number of different channels. The most significant is generally the impact that the policy has on the individuals, businesses or organisations that are directly affected by the policy. These impacts are referred to as direct or first round effects and are routinely included in PBO costing estimates.

In any economic system, however, there are often flow-on effects from a given policy change to other prices and markets which, in turn, can affect budget outcomes. These impacts are referred to as broader economic effects, second round effects, or indirect effects. While there is no question that these broader economic effects do arise, there is generally considerable uncertainty about the magnitude, direction and timing of those effects and their subsequent impact on the Budget.

The approach taken by the PBO to estimate the broader economic effects of policy proposals on the Budget is consistent with the Charter of Budget Honesty Policy Costing Guidelines. That is, in the majority of circumstances budget costings only capture the direct impacts of the policy change, including the behavioural changes of groups who are directly affected by the policy. This is consistent with the approach to most costings undertaken in the United States of America, United Kingdom, Canada and New Zealand.

Every now and then, however, broader economic effects are incorporated in budget projections. Over recent decades there have been seven examples of major reform proposals put forward by Australian governments where broader economic effects have been incorporated.

Consistent with its current approach, the PBO will continue to highlight in its costing responses a qualitative statement when a policy proposal could have material broader economic effects that may affect budget outcomes and cannot be estimated. We will consider incorporating quantitative estimates of broader economic effects into policy costings in limited circumstances where there is compelling evidence of the direction, size and timing of a material economy wide impact, where the way the proposal would be funded has been made clear and where the broader economic impact can be estimated in a cost effective manner.

A key role of the PBO is to prepare costings of policy proposals for all parliamentarians.2 These are estimates of the financial impact of policy proposals on the Australian Government's Budget.

This page expands upon the PBO’s general approach to costings as set out in What is a Parliamentary Budget Office costing? and, in particular, to explains our treatment of potential broader economic effects in costings.

We outline, at a high level, the different ways in which a policy proposal can affect the budget. We consider why quantitative estimates of the broader economic impacts of proposals are rarely included in costings. Next we look at cases where broader economic effects have been included in costings of major policy reform packages in Australia and the reasons for doing so. Finally we set out the approach we use to determine whether and/or how to capture broader economic impacts in our costings.

How does a policy proposal affect the budget?

PBO costings are designed to capture the impact on the Budget of a particular policy proposal being implemented. This is the difference between the estimated budget outcome if a policy proposal were implemented and the estimated budget outcome as published in the most recent economic and fiscal outlook report.3

These costings generally cover a future time period of 10 years and are prepared with reference to the same economic forecasts, parameters and fiscal estimates as presented in the most recent budget update. PBO costings use the same approaches and costing conventions as recommended in the Charter of Budget Honesty Policy Costing Guidelines.4

Conceptually, the budget impacts of a policy proposal can be divided into three broad components:

- The direct static impact of the proposal. This is sometimes referred to as the 'day after' impact of the policy proposal. It assumes there is no response to the policy change on the part of those affected by it and is an element of all costing analyses.

- The direct behavioural impacts of the proposal, which takes account of changes in behaviour by individuals, businesses or organisations directly affected by the proposal and includes impacts on closely related industries.

- Broader economic impacts (or second round effects5) which refer to the impacts on the Budget that arise from the further economic feedbacks from a policy change, for instance due to changes in prices, wages or employment levels flowing on from the introduction of a new policy.

Examples of direct impacts and broader economic effects are set out in Box 1, using the example of an increase in the tax on wine.

Generally, PBO costings include the static and direct behavioural impact of proposals but, with a few exceptions, the PBO has not included quantitative estimates of broader economic effects in its costings.6

The exclusion of broader economic effects from costings has sometimes been criticised as presenting a potentially misleading estimate of the impact of policy proposals on the Budget.7 For instance, on occasions it is argued that costings fail to take account of the stimulatory impact of proposals which, in turn, would help offset the cost of the proposed policy.8 At its most extreme, it is argued that there would be some instances where a reduction in a tax rate results in an increase in Government revenue.9 Or, alternatively, that an increase in Government expenditure (on education, for example) is more than paid for by the Government revenue that is generated from the additional growth that eventuates.

Box 1: Examples of direct impacts versus broader economic effects

This box illustrates a range of potential direct and broader economic effects of a policy change, using the example of an increase in the tax levied on wine called the wine equalisation tax (WET):

Direct effects |

Broader economic effects |

|---|---|

|

|

Estimates of the broader economic effects of a policy proposal on the budget, however, are very challenging to robustly estimate and are more likely to be contested than the direct impacts. In most cases they are also likely to be much smaller in magnitude than the direct impacts. These arguments are considered in more detail below.

Before proceeding further, it is important to emphasise that the PBO’s approach to estimating policy costings should not be taken to imply that we consider the broader economic effects of policy proposals to be unimportant. Pursuing reforms to improve living standards and the efficiency of the economy should always be a priority for Government. The purpose of policy costings is to provide one input into the policy debate, which is the best estimate of the budget cost of the policy proposal over the period ahead. This needs to be considered alongside other factors, including, importantly, the ultimate objective and likely effectiveness of the proposed policy.

Why broader economic effects are rarely included in policy costings

Broader economic effects are generally not included in policy costings because the magnitude of those impacts on budget outcomes is judged to be much smaller and more uncertain than the direct budget cost of the policy proposal, particularly over standard budgetary horizons.

Four specific issues associated with estimating the broader economic impacts of a proposal on the budget are:

- Timeframe: broader economic impacts often take a considerable time to materialise and have little material impact over standard budgetary horizons.

- Uncertainty: there are considerably higher levels of uncertainty in terms of the direction, size and timing of broader economic impacts, as these depend on the responses of, and interactions between, individuals and different sectors in the economy.

- Financing: to accurately assess the broader economic impacts of a particular policy proposal it is critical to take into account how the proposed policy is to be funded. This is often not specified in a policy proposal.

- Risk of double counting: the inclusion of broader economic impacts in individual costings risks double counting because the macroeconomic forecasts that form the basis of costings already include implicit assumptions about ongoing policy reform.

There is an extensive body of literature canvassing issues related to the inclusion of broader economic effects in costings.10 More detail on the approach to estimating these effects in similar jurisdictions can be found in the Appendix. The rest of this section outlines the findings of this literature around the four themes outlined above.

The timeframe for broader economic effects to eventuate is often protracted

The full direct fiscal impact of a policy proposal is generally evident within a year or so of it being implemented, with some behavioural impacts being evident ahead of commencement. On occasions, it will take longer for the full direct impact of the policy to be evident, but rarely would this extend beyond a ten-year horizon.

The broader economic effects of a proposal on the Budget, in contrast, can take a considerable time to eventuate, and an even longer time to reach their full effect. The time taken for such effects to occur means that even when they are significant in relation to the direct impacts of a proposal, the magnitude of those impacts may not be significant within the four-year Budget estimates period or over the ten-year 'medium term'.

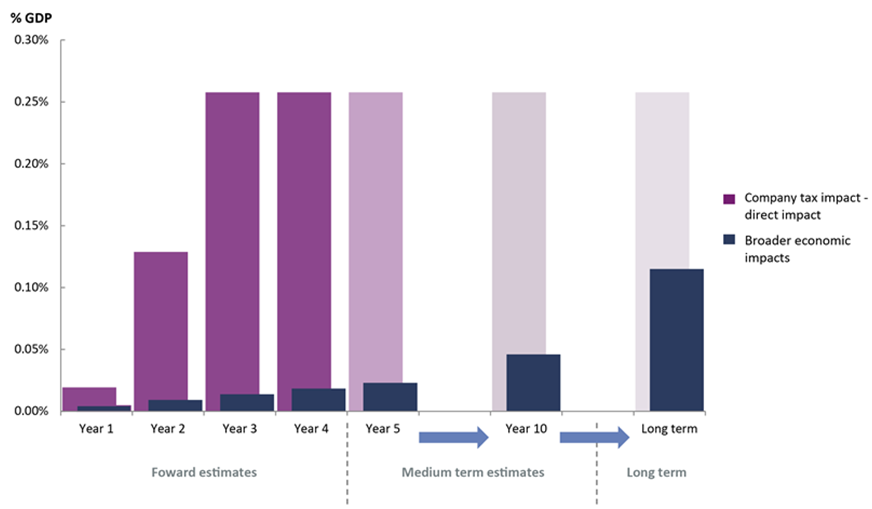

Box 2 illustrates this point with an example based on the 2010–11 Budget. In the 2010–11 Budget, the Government proposed a 2 per cent reduction in the company tax rate financed by the introduction of a resource rent tax, and the budget papers estimated that there would be a 'growth dividend' associated with this policy proposal. In this case, the 'growth dividend' was estimated to arise from increased business investment which was assumed to then flow through into higher business profits and wages in the economy. The higher level of economic activity was, in turn, expected to result in higher tax revenues.

The red bars in Figure 1 show the fully-phased-in cost of the estimated direct impact of the tax cut at just over 0.25 per cent of Gross Domestic Product (GDP) per year. The tax cuts would have commenced from 2013–14, phased in over two years and some of the cost was expected to be brought forward into 2012–13 due to companies shifting income, where possible, to take advantage of the tax cut.

The blue bars in Figure 1 show the estimated budget improvements that were expected to flow from the ‘growth dividend’ the tax cut would generate. In this instance, the ‘growth dividend’ was expected to take up to 25 years to fully materialise, at which time it would offset somewhat less than half the annual reduction in company tax. This figure shows that over both the four years of the budget forward estimates period and over a 10-year horizon, the direct impacts of the tax cut were expected to have the most material impacts on the Budget.

The reason why broader economic effects generally take time to eventuate is because they rely upon significant structural changes taking place in the economy. Efficiency gains from investment decisions, for example, would not have their full economic impact realised until the capital stock of the economy had been renewed, which takes several decades.11 Similarly, the returns from human capital investments (such as improved education outcomes) would have a lag of a decade or more to begin to show benefits (as students enter the workforce), with the full benefits taking a lifetime to be realised.12

Box 2: Timeframe – the magnitude of direct static impacts versus the broader economic impacts

The 2010–11 Budget included estimates of the growth dividend from a cut in company tax from 30 per cent to 28 per cent in two annual steps commencing from the 2013–14 income year. This cut, financed by the introduction of a resource rent tax, was estimated to increase long run GDP by 0.4 per cent per year. In turn, the increase in GDP was expected to produce a long run revenue growth dividend of around 0.1 per cent of GDP per year.

Figure 1: Magnitude of direct versus broader economic impacts

Even where proposals may be expected to have a more immediate impact on behaviour—such as proposals that encourage a change in the supply of labour—the timing of the broader economic effect would depend on how and when this translated to a net increase in employment and hence tax collections.13 These transmission lags mean that even where the broader economic effects are material, the scale of the impact could be uncertain over the forward estimates period and the medium term.

There is considerable uncertainty around assessments of broader economic impacts

The PBO is open about the fact that all costing estimates are subject to uncertainty and we include in our costing responses an explanation of the sources of uncertainty associated with each costing.14 Where relevant, these explanations include a qualitative assessment of whether the particular policy proposal would be expected to have broader economic impacts which could affect budget outcomes.

While uncertainty about the direct impact of a policy proposal essentially depends on the available data and information on the likely behavioural responses of the individuals directly affected by the policy, there are many more sources of uncertainty that affect estimates of the broader economic effects.15 This is because the potential flow-on effects from a policy proposal are many and varied, can have offsetting impacts on the budget and do not eventuate over the same time period. As a result, at any particular point in time it can be uncertain whether the net outcome of the broader economic effects is positive or negative for the Budget. Furthermore, the flow-on economic effects will not necessarily be constant over time, as they will depend on the broader state of the economy.

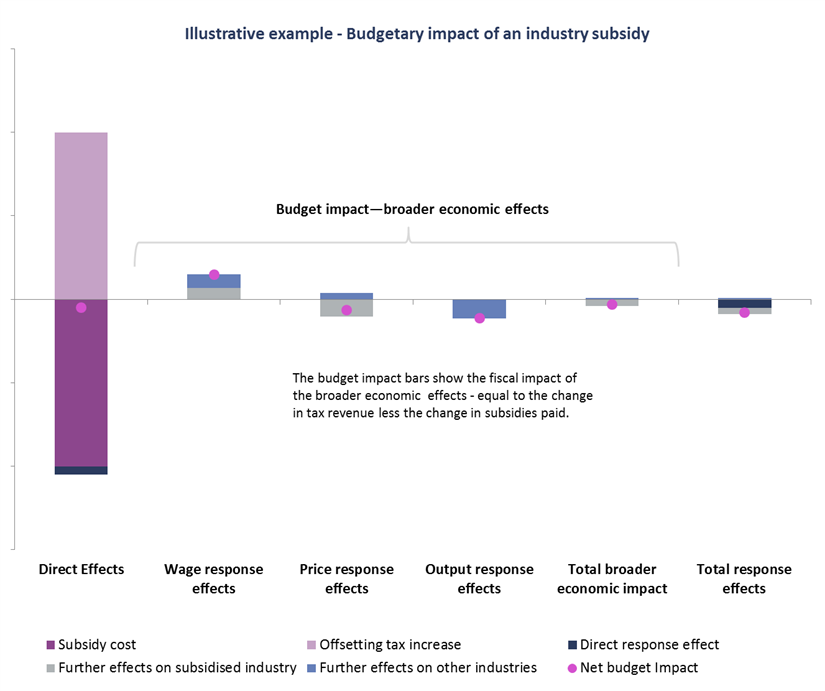

Consider, by way of an example, a policy proposal to provide a production subsidy to the electric bicycle (e-bike) industry. Assume that the economy is operating at close to full employment, with the subsidy being financed by an increase in the general corporate tax rate.

- The production subsidy should reasonably be expected to lead to an increase in employment and output of the e-bike industry (direct impacts) and give rise to flow‑on economic impacts. These flow-on effects may include higher wages for employees of the e-bike industry, depending on the competitiveness of the labour market, and lower prices for the outputs of the e-bike industry, depending on the competitiveness of this industry and the existence of substitute products.

- With the economy operating at full employment, the increase in employment in the e-bike industry is met by hiring workers away from other industries. This means that other industries would either have to reduce employment or increase wages to retain workers, or some combination of both. This would reduce output, profits and investment in the unsubsidised industries, offsetting to some (greater or lesser) extent the increase in output of the e-bike industry. The higher corporate tax rate (which is paying for the production subsidy) would, in turn, be expected to reduce aggregate investment, wages and output.

- The final outcome for the Budget is uncertain. However, in the presence of efficient markets and diminishing returns to investment, theory would suggest that the outcome would be a net reduction in output and most likely a negative impact on the Budget in the long‑run. While there may be an overall positive effect on the e-bike industry, this effect may be more than offset by negative impacts elsewhere.

Box 3 illustrates this example graphically.

Box 3: A production subsidy to the electric bicycle (e-bike) industry to illustrate that further economic impacts can be many and offsetting

The first column in Figure 2 illustrates that the direct effect on the Budget of the increase in the corporate tax rate is roughly offset by the cost of the subsidy. The next three columns illustrate that the impacts on the Budget of the broader economic impacts on wages, prices and output are offsetting, so the total broader economic impact (shown in column 5) is close to zero. The final column shows the net budget impact of both the direct effects and the broader economic impact, which again is considerably smaller than the initial cost of the subsidy.

Figure 2: Further economic impacts can be many and offsetting

The impacts shown in this figure may take many years to eventuate, with some effects flowing through more rapidly than others. The analysis of the impact will also depend on assumptions about the dynamics of individual markets and the interactions between markets. This leads to high levels of uncertainty around the size and timing of budget impacts.

Uncertainty around estimates of the broader macroeconomic impacts of policy proposals is illustrated by the fact that, in many cases, different macroeconomic models generate widely varying estimates of the impact of a given policy proposal. These vary depending on the modelling approach adopted and the assumptions underpinning the model, and can result in the conclusions from any particular model being contested.

More generally, estimating the full suite of economic impacts of a policy proposal typically requires substantial modelling capability, such as a Computable General Equilibrium (CGE) model or a Macroeconometric Model. Like all models, each of these has their advantages and disadvantages and relies upon a combination of economic theory and empirical estimates. But few of these models have been specified in sufficient detail to reflect how individual markets or policy proposals work, meaning that the results of the model may not be representative of the policy proposal itself.16 This lack of detail in the structure of most macroeconomic models presents a further source of uncertainty surrounding estimates of the broader economic impact of proposals.

Finally, uncertainty surrounding broader economic impacts of policy proposals will be more significant when there has been no prior experience of a proposal or where the proposal involves a very substantial change to current policy parameters. In the latter case, transitional impacts could be very large and long lasting, and depend significantly on implementation details.

How proposals are funded matters when assessing broader economic effects

All policy proposals that have an impact on the Budget have to be financed in one way or another. A proposal can be financed by a specific set of saving or revenue raising proposals or it can be financed via a higher budget deficit or lower surplus with a corresponding impact on the level of Government debt. Where a spending proposal is financed by an increase in Government debt, the increase will ultimately have to be repaid, implying that taxes in the future will be higher than they would otherwise have been.

When considering the broader economic impacts of a policy proposal, it is therefore important to take into account how the proposal is to be funded. There is a substantial body of literature expressing concern that the inclusion of the broader economic effects of a proposal in isolation of how it would be funded would present a misleading picture of its aggregate fiscal impact.17 Similarly, for revenue raising proposals, how the funds raised are proposed to be utilised also matters.

For example, while the imposition of a tax, looked at in isolation, would typically result in a welfare loss to the economy through reduced economic efficiency (reducing the gain in revenue), this analysis is incomplete without consideration of how the revenue raised by the imposition of the tax would be used:

- If the revenue from the tax was used to reduce or abolish a different tax, the net macroeconomic impact of the proposal would depend on the relative efficiency of the tax being removed compared with the tax being imposed.

- If revenue from the tax was used to increase Government spending, the net macroeconomic impact would depend on the extent to which this spending increased the productive capacity of the economy compared with the efficiency cost of the tax.

Requiring that policy makers specify how a particular policy proposal is to be financed as part of an assessment of its broader economic effects will also, generally, reduce the size of these second round effects. This is because the direct and broader economic impact of the original policy proposal will usually have the opposite impact on the Budget of the proposed policy to finance the proposal (as illustrated in Figure 2 above).

Potential for double counting

As outlined in Section 2, policy costings are designed to capture the impact on the Budget of a particular policy proposal being implemented. When we consider estimates of the broader economic impact of proposals, however, it is important to understand the assumptions that underpin the existing macroeconomic projections used in the Budget.

For instance, the Australian Government’s economic projections include a technical assumption that labour productivity growth will remain at the average level that has been achieved over the past 30 years. This is a period that includes the surge in productivity growth in the 1990s attributed, among other things, to a period of economic reform in the 1980s and 1990s.18 Implicitly, this assumption therefore implies that productivity dividends from as yet unspecified ongoing reforms of a similar magnitude to those over the past three decades will continue over the medium term.

In essence, the assumptions underlying the Budget effectively require an ongoing level of productivity enhancing reforms just in order to meet the Budget forecasts. This means that including the macroeconomic effect of productivity enhancing reform in the costing of a particular proposal risks double counting, resulting in a misleadingly positive picture of the overall budget position. Keeping track of how much of the baseline productivity enhancement has already been accrued on a proposal-by-proposal basis would be a task that rates on a scale somewhere between difficult and near impossible. A more sustainable approach would be to assume that most of the productivity enhancing potential of measures included in a budget are likely to be necessary to meet the technical assumption rather than including the productivity benefits in the costings of individual proposals.

Similar considerations apply in relation to other broader economic effects, such as impacts on prices, wages and aggregate demand. Forecasts based on historical trends include an implied assumption that the drivers of those trends continue. Where those drivers reflect past policy initiatives, trend-based forecasts effectively assume that there will be a continuation of new policy initiatives to maintain the momentum that underpins the trend. Including estimates of broader economic impacts in policy costings therefore runs the risk of double counting impacts that are already included in the costing base.

The timeliness versus materiality tradeoff

The complexity of estimating economy‑wide effects of policy proposals, as outlined in the sections above, means that their routine inclusion in policy costings could be expected to add very significantly to the time taken and resources required to complete PBO costings. As the United States Congressional Budget Office (CBO) has noted19:

Analyzing the effects on the overall economy of changes in federal fiscal policies—that is, policies governing taxes and spending—requires complex modelling and a significant amount of time.

A key question then is whether the potential benefits of including macroeconomic effects in costings outweigh these costs—and, if so, when.

The evidence suggests that in most cases where the broader economic impact can be estimated, the impact of including broader economic effects would not be sufficiently material on either the costing or the aggregate budget position to justify the time and resources involved.

However, there will be some, rare, exceptions to this rule for major policy packages where there is compelling evidence on the direction, size and timing of material broader economic impacts.

When broader economic impacts have been included in costings

Above we explained why costings (those produced by both the Government and the PBO) generally include both the direct static impact and direct behavioural impact of proposals but rarely include estimates of broader economic impacts. This section looks at the cases where estimates of the broader economic impacts of proposals (or policy packages) have been included in budget estimates and the reasons for doing so.

The most frequent example of a situation where the broader economic impact of a policy is included in a costing estimate is where the policy is expected to have a direct and significant impact on the CPI. These impacts are routinely captured because there is a well-defined legislated link between CPI inflation and the indexation of a number of significant payments and taxes, and the magnitude of these impacts can be significant.

Further economic impacts have also been included in the Australian budget estimates on a number of occasions, often as separate line items in the Budget representing 'growth', 'efficiency' or 'compliance' dividends of a full package of measures. This has generally been done where the Budget has included a significant package of economic reforms that are expected to result in increases in productivity, employment or efficiency, which are in turn expected to result in increases in economic activity which flow back to the Budget through increases in revenue.

Situations where the broader economic impacts of policy proposals have been included in budget aggregates over the past 25 years are:

- The 1994 Working Nation policy

- The 1999 Review of Business Taxation

- The 2000 A New Tax System

- The 2005 Welfare to Work package

- The 2010 Stronger, Fairer, Simpler package

- The 2011 Clean Energy Future package

- The 2013 Repeal of the Carbon Tax.

The broader economic impacts incorporated into the budget aggregates for these packages have related to economy‑wide effects, particularly on labour supply or economic efficiency. A common feature of many of these reform packages was that they were intended to deliver improvements in economic efficiency and were expected to be broadly budget neutral over the relatively short timeframe of the budget forward estimates period.

The common elements in all these cases are that they have all generally been:

- large packages of measures involving significant amounts of expenditure and revenue (in absolute terms)

- broadly budget neutral packages, so that elements that reduce tax or increase expenditure have been broadly matched by other elements that increase tax or reduce expenditure

- reforms aimed at enhancing economic efficiency by improving resource allocation, workforce participation, improving efficiency in taxes, or enhancing savings and investment.

Table 1: provides more detail of these packages and the types of broader economic impact they incorporated.

| Year | Package name | Description of package and further economic impact | Impacts included |

|---|---|---|---|

| 1994 | Working Nation | Labour market reform package expected to increase employment.20 | Costings included savings on social security payments (from reduced unemployment benefits) as an offset to the cost of labour market measures. |

| 1999 | Review of Business Taxation (Ralph Review) | Economic growth dividend from improved resource allocation.21 | Increased economic growth driven by a more efficient tax system was expected to increase Australian Government revenue generally. This impact was not attributed to individual measures in the package. |

| 2000 | A New Tax System | Economic growth dividend from ‘enhanced GDP flowing from the lower cost of investment and a more efficient allocation of resources’ and flow‑on effects to the CPI.22 | Increased economic growth driven by a more efficient tax system was expected to increase Australian Government revenue generally and the impact on revenue was not allocated to individual measures in the package.23 The flow-on effect of higher inflation to price-linked payments and taxes was also reflected in estimates.24 |

| 2005 | Welfare to Work | Welfare system reforms package to encourage increased workforce participation for those with the capacity to work and higher employment over time.25 | These effects were incorporated into the macroeconomic forecasts underpinning the Budget and were not separately identified. |

| 2010 | Stronger, Fairer, Simpler | Tax reforms that included the introduction of a resource super profits tax, replacement of state mining royalties and a reduction in the company tax rate which were expected to increase GDP growth due to increased investment and improved resource allocation.26 | The 2010–11 Budget included a revenue growth dividend arising from an expected increase in GDP of 0.7 per cent in the long run, comprising 0.4 per cent from reduced company tax and 0.3 per cent from resource tax reforms, with these increases expected to take decades to accrue. |

| 2011 | Clean Energy Future | Package that included the introduction of an explicit price on greenhouse gas emissions through the carbon pricing mechanism. The forecasts of real GDP growth, employment growth, the unemployment rate and consumer prices incorporated the impact of the carbon price.27 | The introduction of a carbon price was estimated to lead to a one-off 0.7 per cent increase in consumer prices in 2012‑13.28 The flow-on effect of higher inflation to price-linked payments and taxes was reflected in budget projections. Real GDP growth and employment growth were expected to be reduced by less than one quarter of a percentage point in 2012‑13, with no discernible impact on the forecast unemployment rate. |

| 2013 | Repeal of the Carbon Tax | Package that repealed the carbon pricing mechanism and some other elements of the Clean Energy Future package. The package was expected to lower headline and underlying inflation. | Repeal of the carbon price was estimated to reduce the CPI by less than one quarter of a percentage point in 2014-1529 and was 'expected to support household consumption growth in the short term and make a small contribution to national income growth over the longer term.'30 |

Conclusion

Policy costings are designed to capture the impact on the Budget of a particular policy proposal being implemented. These routinely incorporate the direct behavioural impacts of the proposal in addition to the direct static impact, on the basis that behavioural responses can be significant and including these impacts improves the accuracy of the costing estimate without introducing too much uncertainty.

On the other hand, as outlined in this paper, there are a number of reasons to expect that broader economic effects are less likely to have a material impact on costing estimates and are less likely to be able to be robustly estimated.

- the broader economic impacts of a proposal are likely to take a longer time to materialise, so that only a small portion of the effect is likely to be observable within the forward estimates period or over the medium term

- the broader economic impacts can be comprised of a number of effects that move in different directions, such that the overall direction and magnitude of those effects is unclear

- the way in which a proposal is financed matters and financing has its own offsetting broader economic impact, so the sum of the broader economic impacts of the proposal and its financing method is generally much smaller than the estimate of the broader economic impact of the initial proposal

- in many cases, the budget estimates may already include allowance for ongoing policy reforms, with the effect that the broader economic impact of a proposal has already been taken into account and including a further provision would result in double counting.

Consistent with the Charter of Budget Honesty Policy Costing Guidelines, the PBO’s costings will continue to primarily capture the direct budgetary impacts of policy proposals, including direct behavioural responses, and will not generally take broader macroeconomic effects into account. We will, however, routinely capture the flow-on budgetary effects of changes in the inflation rate, where this can be robustly estimated.

We will also continue, where appropriate, to supplement the documentation in our costing responses with qualitative statements on the potential broader economic impact of proposals which may affect budget outcomes where these are likely to be material.31

In limited circumstances, the PBO will consider incorporating broader economic effects into costings where there is compelling evidence of the direction, timing and magnitude of the macroeconomic effect, the impact is expected to be material to the costing, and the funding of the package is specified. This analysis would be expected to ensure that there is no double counting of economy‑wide effects and would only be conducted if it is assessed that the impacts can be estimated in a cost‑effective manner.

Appendix—International practice

This appendix provides a brief summary of approaches taken in the United States of America, United Kingdom, New Zealand and Canada to account for second round effects in estimates of the budget cost of policy proposals.

The CBO has had a long standing practice (dating back to 1974 when it was established) of not including broader macroeconomic effects in its cost estimates of legislative proposals. A key concern of the CBO was that—as the net macroeconomic impact of a policy proposal would depend on how it was funded—this would require them to make assumptions about the future policy decisions, where differing assumptions could change the direction, not just the magnitude, of the net macroeconomic effect.32

In May 2015, the Congress adopted a concurrent resolution33 requiring the CBO, to the greatest extent practicable, to incorporate macroeconomic effects into its 10-year cost estimates for 'major legislation'—defined as having a gross budgetary effect of 0.25 per cent of GDP (excluding macroeconomic feedback) in any year over the next 10 years (an amount equal to about $US47 billion in 2016).34 The resolution also required these estimates to include, when practicable, a qualitative assessment of the budgetary effects for the following 20 years.

It remains relatively rare for the CBO to include macroeconomic effects in its costing estimates, reflecting the high threshold for the Congressional resolution to apply. Moreover, the CBO was unable to include macroeconomic effects in its costing estimate of the American Health Care Act of 2017, despite it being above the 'major legislation' threshold, as it was not practicable due to 'the limited time available' to prepare the costing.35

The costings assessed by the United Kingdom Office of Budget Responsibility (OBR) do not include macroeconomic effects. Policy costings only include static impacts, and 'first round' and microeconomic behavioural responses.36

The OBR note that, in practice, the majority of policies are too small to allow effects to be quantified policy‑by‑policy in a meaningful way. The OBR state that a challenge in using CGE models for dynamic scoring 'is the amount of evidence required to estimate the behavioural features of the model', as 'in practice, like any model it is a partial and simplified representation of prices and quantities in the economy'.37

However, in preparing its economic and fiscal projections the OBR takes into account broader macroeconomic effects of policy measures in a fiscal update where they are identifiable and quantifiable. In undertaking this analysis, due to time and resource constraints, OBR uses a top down approach rather than seeking to separately assess the macroeconomic impact of every single policy measure. The focus of the OBR assessment is on macroeconomic level behavioural effects of large policies and/or the aggregate impact of the net impact of policy proposals announced in a fiscal update.

Much of the focus of the OBR’s analysis of indirect effects is on the short term impact on aggregate demand rather than the long term impact on productivity. The OBR note that long term economic effects are subject to significant uncertainty, and that projections of potential growth are based on historical trends that 'implicitly embody the past effects of policy measures on productivity growth'.38

New Zealand Treasury's fiscal costings focus on the 'initial impact of proposals on the key fiscal aggregates over the [five year] forecast horizon'. Macroeconomic or second round effects are excluded from estimates of the fiscal impacts of policy proposals, 'due to inherent uncertainty over their timing and impact'.39

New Zealand Treasury draws a distinction between economic analysis of policy proposals and fiscal costings. Where long-run economic analysis produces materially different results from the short run fiscal costing (eg due to macroeconomic effects), these reports are generally identified and reported separately.

An appendix to the guidance for the 2017 election period issued by the New Zealand State Services Commission provides guidelines for costing party political policies.40 The guidance notes that costings of proposals should be limited to the factual data readily available in the Treasury and other agencies, and should be documented in full, including a clear explanation of all sources and of any assumptions made, and should avoid additional commentary, value judgements and unreasonable technical assumptions.

The Canadian Office of the Parliamentary Budget Officer (CPBO) does not include macroeconomic effects in its costings of individual pieces of legislation. As with other countries, this is because there are a wide range of possible views on the macroeconomic effects of any given policy proposal and because they judge that, in most cases, it would not make a difference to the impact or views of the merits of the policy proposal.41 The CPBO also notes that incorporating macroeconomic effects in costing estimates would be labour intensive.

Footnotes and references

- Ceased working with the PBO on 2 June 2017.

- Section 64E, Parliamentary Service Act 1999.

- Usually the annual Budget or the Mid-Year Economic and Fiscal Outlook (MYEFO).

- Sections 64E(3) and 64G, Parliamentary Service Act 1999.

- In the United States, the inclusion of second rounds effects in policy costings is sometimes referred to as dynamic scoring.

- The principal exceptions have been costings of policies which have a measurable direct impact on the CPI which would flow automatically through to indexed welfare benefits and certain excise revenues, where these automatic flow through effects have been included in the costing estimates. A number of examples of this approach are included in PBO (2013), PBO (2015) and PBO (2016).

- See, for example, Auerbach (1996, 2005), Mankiw et al (2006), Elmendorf (2015). The recent independent review into the PBO noted that 'several stakeholders suggested that the PBO should include economy wide effects in policy costings': Watt and Anderson (2017). The recent review of economic modelling at the Treasury also recommended it 'consider whether, in estimating the budget impact from a tax policy change, it takes into account potential economy-wide effects': Murphy (2017).

- While most commonly referred to as the Laffer Curve, this concept has a long history, with the idea being referred to in the writings of Adam Smith, Edmund Burke, Jules Dupuit and John Maynard Keynes amongst many others: Blinder (1981); Fullerton (1982); Laffer (2004).

- Technically, where there are two tax rates at which no revenue is raised (with one being where the tax rate is zero and the other being the point where the tax base is zero) then there must be an intervening point at which the marginal revenue from a change in the tax rate becomes negative. This is a standard result reported in microeconomic and public finance texts—see for example Varian (1999) and Rosen and Gayer (2013). The controversy attached to this view relates more to assertions about where a country (or a tax) is on the Laffer curve—which is an empirical question.

- See, for example, Auerbach (1996, 2005), CBO (2002a), Furman (2006), Mankiw et al (2006), Adam et al (2009), The Committee for a Responsible Federal Budget (2012) and Elmendorf (2015).

- See, Cao et al. (2015); Kouparitsas et al. (2016); KPMG (2016).

- OECD (2015), p. 16.

- Noting that a net increase in the labour supply does not automatically translate to a net increase in employment.

- PBO (2017).

- See, for example, CBO (2002a), Furman (2006), Adam et al (2009), The Committee for a Responsible Federal Budget (2012), Huang et al (2015), The Charter of Budget Honesty Policy Costing Guidelines p. 7, Brown (2007).

- See, for example, Altshuler, et al (2005).

- See, for example, CBO (2002a), Furman (2006), Adam et al (2009), The Committee for a Responsible Federal Budget (2012).

- PBO (2014).

- CBO (2014).

- Keating (1994).

- Review of Business Taxation (1999), p. 695.

- Costello, (1998), p. 16 and 30.

- ibid, p. 34 and 35.

- Costello, (1998), p. 16 and 2000-01 Australian Government Budget – Budget Paper No. 1 at p. 3-13 to 3-19.

- Costello (2005) and the 2005-06 Australian Government Budget.

- 2010-11 Australian Government Budget—Budget Paper No. 2 at p. 48. The growth dividend was reduced after taking into account changes to the resource super profits tax announced on 2 July 2010 (2010 Australian Government Economic Statement at p. 23, 24, 28; 2010–11 Australian Government Mid Year Economic and Fiscal Outlook at p. 228).

- 2012-13 Australian Government Budget—Budget Paper No. 1 at p. 2-36 (Box 8 of Statement 2).

- Ibid.

- 2013-14 Australian Government Mid-Year Economic and Fiscal Outlook at p. 12.

- Ibid.

- The PBO costing minute in relation to the Australian Greens proposal to replace stamp duty with a broad based land tax—published here by the Australian Greens—stated that: 'The 2009–10 Australia’s Future Tax System review highlighted that a broad based land tax is a more economically efficient tax than stamp duty. This implies that replacing stamp duty with a broad based land tax would increase economic activity over the medium to long term. As tax revenue generally increases in line with economic activity, this would be expected to increase taxation revenue over time. However as the timing and magnitude of the macroeconomic impact of the proposal would be highly uncertain, the PBO has not included it in the costing.'

- Former CBO director Dan Crippen expanded on these points in evidence before the US House of Representatives Committee on the Budget in May 2002: see CBO (2002a), (2002b).

- https://www.cbo.gov/publication/50357

- In Australia, this would be equivalent to a policy proposal having a gross budgetary effect of around $4 billion in 2016–17.

- CBO (2017).

- OBR (2014).

- Ibid.

- Ibid.

- New Zealand Treasury (2017).

- New Zealand State Services Commission (2017).

- Flavelle (2015).

Adam, S & Bozio, A 2009, ‘Dynamic Scoring’, OECD Journal on Budgeting, vol. 2, pp. 1-26.

Altshuler, R, Bull, N, Diamond, J, Dowd, T & Moomau, P 2005, 'The Role of Dynamic Scoring in the Federal Budget Process: Closing the Gap between Theory and Practice', American Economic Review, vol. 95, no. 2, pp. 432‑436.

Auerbach, A 1996, 'Dynamic Revenue Estimation', Journal of Economic Perspectives, vol. 10, no. 1, pp. 141‑157.

Auerbach, A 2005, 'Dynamic Scoring: An Introduction to the Issues', American Economic Review, vol. 95, no. 2, pp. 421‑425.

Australian Government 2016, Charter of Budget Honesty Policy Costing Guidelines, Guidelines Issued Jointly by the Secretaries to the Treasury and the Department of Finance, available at: https://www.finance.gov.au/publications/charter-of-budget-honesty/

Blinder, A 1981, 'Thoughts on the Laffer Curve', in The Supply Side Effects of Economic Policy, Meyer L, (ed), St Louis: Center for the Study of American Business at Washington University and Federal Reserve Bank of St Louis, available at: https://research.stlouisfed.org/publications/review/81/conf/1981section1-3.pdf

Brown, C 2007, 'Treasury costings of taxation policy', Economic Roundup, pp. 29-48, available at: http://www.treasury.gov.au/~/media/Treasury/Publications%20and%20Media/Publications/2007/Economic%20Roundup%20Winter%202007/Downloads/PDF/02_Treasury_costings_of_tax_policy.ashx

Cao, L, Hosking, A, Kouparitsas, M, Mullaly, D, Rimmer, X, Shi, Q, Stark, W & Wende, S 2015, 'Understanding the Economy-wide Efficiency and Incidence of Major Australian Taxes', Treasury Working Paper 2015-01, The Treasury, Canberra.

The Committee for a Responsible Federal Budget 2012, Understanding Dynamic Scoring, Washington, available at http://www.crfb.org/papers/report-understanding-dynamic-scoring.

Congressional Budget Office 2002a, Federal Budget Estimating, Statement before the Subcommittee on Legislative and Budget Process Committee on Rules, US House of Representatives, Congressional Budget Office, available at: http://www.cbo.gov/sites/default/files/cbofiles/ftpdocs/34xx/doc3422/05-09-fedbudestimating.pdf

Congressional Budget Office 2002b, Supplement to CBO’s May 9 2002 Testimony on Federal Budget Estimating, Statement before the Subcommittee on Legislative and Budget Process Committee on Rules, US House of Representatives, available at: http://www.cbo.gov/sites/default/files/cbofiles/ftpdocs/35xx/doc3511/05-09-02-supplementtestimony.pdf

Congressional Budget Office (2012), How the Supply of Labor Responds to Changes in Fiscal Policy, available at: https://www.cbo.gov/sites/default/files/112th-congress-2011-2012/reports/43674-laborsupplyfiscalpolicy.pdf

Congressional Budget Office (2014), How CBO Analyzes the Effects of Changes in Federal Fiscal Policies on the Economy, available at: https://www.cbo.gov/sites/default/files/113th-congress-2013-2014/reports/49494-FiscalPolicies.pdf

Congressional Budget Office (2015a), CBO’s Approach to Dynamic Analysis, Presentation by Ben Page, Chief, Fiscal Policy Studies Unit, to National Tax Association 108th Annual Conference on Taxation, available at: https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/presentation/51021-dynamicanalysis.pdf

Congressional Budget Office (2015b), Answers to Questions about Dynamic Analysis, CBO Blog, available at: https://www.cbo.gov/publication/50357

Costello, P 1998, Tax Reform – not a new tax a new tax system, Australian Government Publishing Service, Canberra.

Costello, P 2005, Welfare to Work Package, Press Release 042-2005, available at: https://ministers.treasury.gov.au/DisplayDocs.aspx?doc=pressreleases/2005/042.htm&pageID=003&min=phc&Year=2005&DocType=0

Dawkins, J 1992, Security in Retirement, Australian Government Publishing Service, Canberra

Elmendorf, D 2015, 'Dynamic Scoring: Why and How to Include Macroeconomic Effects in Budget Estimates for Legislative Proposals', Brookings Papers on Economic Activity, pp. 91-149.

Feldstein, M 2008, 'Effects of Taxes on Economic Behavior', The National Tax Journal, vol. LXI, no. 1, pp. 131-39.

Flavelle, C 2015, Who's Right on Dynamic Scoring? Ask Canada, Bloomberg View, available at: https://www.bloomberg.com/view/articles/2014-12-31/whos-right-on-dynamic-scoring-ask-canada

Fullerton, D 1982, 'On the Possibility of an Inverse Relationship between Tax Rates and Government Revenues', Journal of Public Economics, vol. 19, no. 1, pp. 3-22.

Furman, J 2006, A Short Guide to Dynamic Scoring, Center on Budget and Policy Priorities, available at: http://www.cbpp.org/files/7-12-06bud2.pdf

Keating, P 1994, Working Nation: the White Paper on Employment and Growth, Australian Government Publishing Service, Canberra.

Kouparitsas, M, Prihardini, D & Beames, A 2016, Analysis of the Long Term Effects of a Company Tax Cut, Treasury Working Paper 2016-02, available at: http://www.treasury.gov.au/PublicationsAndMedia/Publications/2016/working-paper-2016-02

KPMG 2016 'Modelling the Macroeconomic Impact of Lowering the Company Tax Rate in Australia', KPMG Economics.

Laffer, A 2004, The Laffer Curve: Past, Present, and Future, The Heritage Foundation Backgrounder No. 1765 on Taxes, available at: http://www.heritage.org/research/reports/2004/06/the-laffer-curve-past-present-and-future

Leeper, E & Susan Yan, SC 2008, 'Dynamic scoring: Alternative financing schemes', Journal of Public Economics, vol. 92, no. 1-2, pp. 159-182.

Mankiw, G & Weinzierl, M 2006, 'Dynamic Scoring: A Back-of-the-envelope guide', Journal of Public Economics, vol. 90, pp. 1415 1433.

Murphy, C 2017, Review of Economic Modelling at the Treasury, available at: https://cdn.tspace.gov.au/uploads/sites/99/2017/05/Review-of-Economic-Modelling-at-Treasury.pdf

New Zealand Treasury 2017, Costing of Political Party Policies, available at: http://www.treasury.govt.nz/publications/guidance/planning/costingpolicies

New Zealand State Services Commission 2017, Guidance for the 2017 Election Period: State Servants, Political Parties, and Elections Appendix 2: Guidelines for Costing Party Political Policies, available at: http://www.ssc.govt.nz/appendix-2-guidelines-costing-party-political-policies

Office for Budget Responsibility 2014, Policy costings and our forecast, Briefing Paper, No. 6, March 2014, available at: http://cdn.budgetresponsibility.org.uk/27814-BriefingPaperNo_6.pdf

OECD 2015, Universal Basic Skills: What Countries Stand to Gain, OECD Publishing, available at: http://dx.doi.org/10.1787/9789264234833-en

Parliamentary Budget Office 2013, Post election report of election commitments: 2013 general election, available at: https://www.pbo.gov.au/elections/2013-general-election/2013-post-election-report

Parliamentary Budget Office 2014, The sensitivity of budget projections to changes in economic parameters: Estimates from 2014–15 to 2024–25, Report no. 03/2014, available at: https://www.pbo.gov.au/publications-and-data/publications/research-reports/sensitivity-budget-projections-changes-economic-parameters

Parliamentary Budget Office 2015, Goods and Services Tax: Distributional analysis and indicative reform scenarios, Report no. 05/2015, available at: https://www.pbo.gov.au/publications-and-data/publications/research-reports/goods-and-services-tax

Parliamentary Budget Office 2016, Post election report of election commitments: 2016 general election, available at: https://www.pbo.gov.au/elections/2016-general-election/2016-post-election-report

Parliamentary Budget Office 2017, Factors influencing the reliability of policy proposal costings, Information paper no. 01/2017, available at: https://www.pbo.gov.au/for-parliamentarians/how-we-analyse/factors-influencing-reliability-policy-proposal-costings

Review of Business Taxation 1999, A Tax System Redesigned: More certain, equitable and durable, July 1999, available at: https://rbt.treasury.gov.au/

Rivlin, A 2017, Coping with change at an independent fiscal institution, Keynote address to the 9th annual meeting of OECD Parliamentary Budget Officials and Independent Fiscal Institutions on April 6 2017, available at: https://www.brookings.edu/on-the-record/coping-with-change-at-an-independent-fiscal-institution/

Rosen, H & Gayer, T, 2013, Public Finance: Tenth Edition, McGraw-Hill.

Treasury 2016, Economy wide modelling for the 2016-17 Budget, available at: https://www.treasury.gov.au/~/media/Treasury/Publications%20and%20Media/Publications/2016/Budget%20Modelling/Downloads/PDF/160503_Economy-wide%20modelling.ashx

Huang, CC & Van de Water, P 2015, House 'Dynamic Scoring' Rule Likely Will Mean More Tax Cuts – Not More Information, Center on Budget and Policy Priorities, available at: http://www.cbpp.org/sites/default/files/atoms/files/1-5-15bud.pdf

Varian, H 1999, Intermediate Microeconomics: A Modern Approach: Fifth Edition, W.W. Norton.

Watt, I & Anderson, B 2017, Parliamentary Budget Office Review 2016–17: Report of the Independent Review Panel, March 2017.