Information paper no. 02 | 2017 | Date issued: 30 November 2017

PBO information papers are published to help explain, in an accessible way, the underlying data, concepts, methodologies and processes that the PBO uses in preparing costings of policy proposals and budget analyses. The focus of PBO information papers is different from that of PBO research reports which are aimed at improving the understanding of budget and fiscal policy issues more broadly.

Overview

Every year, we prepare a large number of policy costings for parliamentarians. In 2016–17, for example, we prepared over 1,600 policy costings. Each costing provides an estimate of the proposed policy’s financial implications on the Australian Government Budget over the next decade.

Our objective is to provide independent costings of policy proposals that can be interpreted in the same way as those presented by the Government in the Budget. PBO costings are therefore prepared to the same standards and using the same concepts as Budget costings. The purpose of PBO costings is to support a more informed policy debate by allowing all parliamentarians to include the financial impact of their policy proposal in their policy development processes.

Our costings present estimates of budget impacts on each measure of the budget balance (fiscal, underlying cash and headline cash) and the Government’s balance sheet, where relevant. These costings include an estimate of the changes to the revenue or expenditure streams directly associated with the policy as well as any changes in departmental resources required to deliver a policy proposal. A disaggregation of the impacts is usually provided to illustrate the impact on different components of the Budget.

PBO costings include the static (‘day after’) and direct behavioural impacts of policy proposals. We generally do not include quantitative estimates of broader economic effects in our costings but provide a qualitative statement about these effects if they are likely to be significant.

There are four key elements of a policy costing:

- the policy specification

- the data and key assumptions informing the costing

- the costing model and methodology

- a summary of the factors affecting the reliability of the costing estimate.

Each of these elements are summarised in PBO costing minutes, in addition to the quantitative estimates of budget impacts, to provide transparency around the costing estimates.

1 Introduction

A key objective of the PBO is to support a more informed policy debate. Part of that objective is achieved by providing services to all parliamentarians to estimate the financial implications, or ‘cost’, of their policy proposals. This aims to help level the playing field by providing access to costing and other analytical services that, in the absence of the PBO, would normally be exclusively available to the Government. The PBO’s estimates are prepared subject to the same rules and conventions as Government budget estimates.

This information paper provides a conceptual explanation of what a costing is, what a costing is designed to capture and how a costing estimate is generated. It has been prepared to improve understanding of what a costing represents and assist in the interpretation of the material that is presented in our costing minutes.

Policy costings prepared by the PBO fall into three categories that reflect the costing functions set out in the Parliamentary Service Act 1999:

- outside the caretaker period of a general election, policy costings are completed following requests from senators and members, with the requests and our responses kept confidential if so directed by the requestor

- during the caretaker period of a general election, policy costings of publicly announced policies are completed following requests from authorised members of Parliamentary parties or independent members. These costings are then publicly released upon completion

- following each general election the PBO prepares a Post Election Report of the budget impacts of the election commitments of designated parliamentary parties (A designated parliamentary party means a party with at least five members in the Parliament immediately before the commencement of the caretaker period for a general election). This report contains costings for policies deemed by the PBO, in consultation with each party, to have been an election commitment.

PBO costings estimate the financial impact of policy proposals on the Budget over the next decade and, consistent with the Charter of Budget Honesty Policy Costing Guidelines, they take account of any significant direct behavioural responses to policy proposals but do not generally include broader economic effects.

Although policy costings completed outside the caretaker period generally remain confidential, we are committed to providing transparency in relation to costing processes. A wide selection of PBO costing minutes are published on our website, including costings for parliamentarians that are no longer confidential and costings contained in the Post-Election Reports for the 2013 and 2016 elections.

The remainder of this paper is structured as follows: Section 2 outlines the purpose of the PBO undertaking costing analyses; Section 3 discusses what a costing is trying to capture and summarises the key conceptual elements of a policy costing; Section 4 outlines the key elements of the process of generating a costing, including the policy specification, the costing methodology applied, the role of assumptions, and the assessment of reliability; and Section 5 summarises the information presented in a costing minute.

2 The role of costings in the public debate

The purpose of a costing is to determine and present the likely financial implications of a proposal on the Budget. The cost of a proposal and its affordability, in the context of Australia’s broader budgetary position, are important issues to take into account as part of the policy consideration process.

The PBO’s independent costing advice helps all parliamentarians compare the costs and the benefits of policy proposals. PBO costings are prepared according to the same standards and concepts as the Government’s budget costings, use the best available data, and can be interpreted in the same way as those presented by the Government in the Budget.

By providing this costing advice, we aim to support those engaged in the public policy debate to focus on the merits of individual policy proposals, how each policy proposal affects the Budget and the net impact on the Budget of a set of policy proposals.

Parliamentarians can request the PBO to undertake a range of other pieces of analysis that are budget related. The purpose of these requests is also to inform parliamentarians and the parliamentary debate. They may include requests for analysis such as:

- the amount included in the budget estimates for particular measures or programs

- projections of budget estimates over different time periods

- the distributional impacts of particular measures or programs across variables such as age, gender, industry, income level and occupation, where the relevant information is available.

This information paper does not cover the PBO’s responses to these broader requests for budget analysis because the subjects of such requests, and the form in which responses may be provided, are too varied. It should be noted, however, that they serve a complementary purpose to costings and that many of the data sources and methods used to respond to requests for costing advice from the PBO can also be applied to these other requests.

3 What does a costing capture?

The costings prepared by the PBO are assessments of the financial impact of proposed policy changes on the Australian Government Budget over the next decade. They estimate how much a policy proposal, if implemented, would change the budget outcome as presented in the most recent Economic and Fiscal Outlook (See Mid-Year Economic and Fiscal Outlook (MYEFO) and Pre-Election Economic and Fiscal Outlook (PEFO)). Given that the budget outcome is the amount by which the Budget is expected to be in surplus or deficit, a costing assesses whether implementation of a given policy proposal would lead the Budget to be more or less in surplus or more or less in deficit.

(The PBO can also prepare responses to requests for budget analysis that compare a policy proposal with a baseline that is different from the most recent budget update. For example the baseline could be determined by a piece of legislation that was passed after the most recent update, changing the baseline from what was assumed in the budget update. Such analyses are called ‘budget analysis’ rather than ‘costings’―they cannot be directly added to line items from the most recent budget update.)

In practice, many policy proposals affect just one part of the Budget. So a school spending costing will mainly focus on the change in expenditure on schools as a consequence of the new policy proposal and a Goods and Services Tax (GST) costing will mainly focus on the change in GST revenue as a result of the new policy proposal. On occasions, a policy proposal will affect a number of different components of the Budget and these will all need to be taken into account. A change in a particular welfare payment, for example, may also affect individual tax receipts or the eligibility for other welfare payments. All of these implications are taken into account in determining the costing.

Conceptually, when simulating the impact of a policy proposal on the Budget, we consider three broad impacts:

- The direct static impact of the proposal. This is sometimes referred to as the ‘day after’ impact of the policy proposal. It assumes there is no behavioural response to the policy change on the part of those affected by it. It is an element of all costing analyses.

- The direct behavioural impact of the proposal. This takes account of changes in behaviour by individuals, businesses or organisations directly affected by the proposal, and includes impacts on closely related industries. Behavioural effects are often included in costing estimates where they are likely to have a measurable impact.

- The broader economic effects (or second round effects) of the proposal. These refer to the impacts on the Budget that arise from the further economic feedbacks from a policy change, for instance due to changes in aggregate prices, wages or employment levels flowing on from the introduction of a new policy.

Examples of direct impacts and broader economic effects are set out in Box 1, using the example of an increase in the wine equalisation tax.

Box 1: Examples of direct impacts versus broader economic effects

This box illustrates a range of potential direct and broader economic impacts of a policy change, using the example of an increase in the tax levied on wine called the wine equalisation tax (WET).

| Direct impacts | Broader economic impacts |

|---|---|

|

The direct static impact. The impact of the proposal on the Budget, before any behavioural impact is included. It is equal to the increase in the WET on wine multiplied by the value of wine sold each year. The direct behavioural impact. A higher tax on wine will increase the price of wine and tend to reduce the volume of wine consumed. This behavioural impact would reduce the revenue raised from the wine equalisation tax. Related behavioural impacts - due to changes in the consumption of close substitute or complementary goods. An increase in WET alone would tend to encourage individuals to switch to consuming other beverages-including beer, spirits and soft drinks-and lead to higher revenue from the direct taxation of these substitute goods. Changes in other taxes directly related to wine consumption. As well as the WET, GST is levied on the value of wine consumption. A change in the value of wine consumption (and consumption of closely substitute products) would therefore affect GST revenue. Changes in Government expenditures directly related to wine consumption. This would capture the change in any other Government expenditures that support wine production and are affected by the reduction in wine consumption that occurs. |

Automatic flow-on impacts. The direct price impact in the WET would have an impact on the consumer price index (CPI) that would flow through into CPI-indexed taxes and payments. Flow on effects on the demand for labour and resources in the general economy. These effects arise as the change in demand for wine affects the demand for labour and resources in the wine industry and this, in turn, affects the demand for labour and resources in other industries. These impact on, for example, wage, employment, investment and profit outcomes, which may in turn affect Government revenue and expenses. Flow on effects on other payments and programs. Changing the WET may affect health outcomes and/or life expectancy. These, in turn, may affect health expenditure and age pension outlays. Flow on effects to economic efficiency. An assessment of the budget impact of the economic efficiency effect of an increase in the tax levied on wine would need to be considered against the budget impact of how additional tax revenue is used. |

Generally, PBO costings focus on the direct static and direct behavioural impacts of policy proposals. With a few exceptions, we have not included quantitative estimates of broader economic effects in our costings as the magnitude of those effects is much smaller and more uncertain than the direct budget cost of the policy proposal, particularly over the standard budgetary horizons. These issues are discussed in more detail on the Including broader economic effects in policy costings page.

4 Elements of the costing process

The PBO has to undertake a number of steps in order to assess the cost to the budget of a policy proposal:

- First, the policy has to be carefully specified to ensure that there is a good understanding of the details of the proposal.

- Second, the methodology for estimating the cost has to be determined. This takes into account the availability of relevant data and the level of detail required for a reasonable estimate to be generated.

- Third, key assumptions have to be made to fill in gaps in the data or information underlying the costing, or to take account of likely behavioural effects.

- Finally, an assessment of the factors affecting the reliability of the costing estimates is made.

The outcome of this process is a costing minute, which provides information on each of these steps and includes an overview that summarises the costing results and any key messages and caveats regarding the costing. The costing minute is intended to be a standalone document.

This section steps through each of these key elements of the costing process and in the next section we provide details on the information that is presented in costing minutes.

4.1 Specification

The specification of the policy proposal to be costed is the starting point for a costing analysis. The costing specification sets out the change to existing policy, or introduction of new policy, that is the subject of the costing analysis and is provided by the individual parliamentarian or political party that requests the costing.

It is important to note that the PBO only costs policy proposals as specified by the parliamentarian who makes the request, so it would be incorrect to represent any costing done for one parliamentarian or party as a PBO costing of the policy of any other parliamentarian or political party. While one policy specification may look similar to another, the financial implications can differ substantially depending upon the policy details.

The policy specification needs to include the following details:

- the aim of the policy change that is being made, which provides the context and helps us understand the policy proposal

- the change that is being made to current policy settings, including details of any changes in:

- grant amounts

- payment rates

- tax rates

- the transactions base

- eligibility criteria

- thresholds

- taper rates

- financing arrangements, and

- any other matter that has a bearing on the financial impact of the proposal.

- implementation details, such as which agency will administer the policy

- the commencement date of the policy

- the date of announcement of the policy

- details of any transitional arrangements

- whether the policy is ongoing or terminating, and if it is terminating, the termination date

- any additional analysis that the requestor would like included in the costing minute.

We always summarise the policy specification for the costing at the start of a costing minute so that it is clear exactly what has been costed.

4.2 Data and assumptions

In order to fully understand the policy specification and the underlying policy framework, and to subsequently undertake the requested costing, the PBO draws upon a range of relevant information, research and data. This information forms the basis of models and assumptions used to undertake the costing, and the quality of this information affects the certainty of the costing estimate.

4.2.1 Data sources

PBO costing minutes provide details of the data and other sources of information used to prepare the costing estimates.

Data are the factual base from which the costing analysis starts. Data are used as the basis for describing the costing base and/or eligible population for a costing analysis. The data used in policy costings can come from a range of sources which can differ significantly in the level of detail.

The data that underpin many costing models will often relate to a period sometime in the past when the data was collected. Our costing models will adjust these data, growing the values by indexing them to representative price and quantity variables to estimate what their values would be in the years presented in the costing.

The PBO is able to access a range of unpublished government data from Australian Government agencies. We have working arrangements with Government departments and agencies through the Memorandum of Understanding between the Parliamentary Budget Officer and the Heads of Commonwealth Bodies in relation to the Provision of Information and Documents (the MOU). The purpose of the MOU is to facilitate the formation of a collaborative, productive and collegiate working relationship between the parties. Data are usually received within five to ten days of a request being made, although some requests may take longer where they require the compilation of more complex data.

An agency head may specify that some or all of that information provided be treated as confidential. Where that is the case, we are required by legislation to protect the information specified from disclosure and will report this in the costing minute.

4.2.2 Key assumptions

Costing models always contain a set of assumptions about matters such as the underlying policy settings or behavioural responses. These assumptions are based on a combination of empirical evidence, theoretical conjecture and professional judgement.

Assumptions are used in costings in a number of roles:

- to fill gaps in the information or data underlying the costing

- to take account of elements in the costing such as the behavioural responses of those affected by a proposal

- as elements in the specification of the structure of the costing model.

The assumptions used in a costing may be explicit or implicit. Explicit assumptions are those where the analyst makes a deliberate choice in setting the value of the assumption, for example an adjustment may be made to account for a specific type and amount of behavioural change. Implicit assumptions are the (less obvious) assumptions embedded in aspects of the costing such as the structure of the model or the methodology used to produce the estimates.

The PBO costing minute summarises the key assumptions that are made in the costing of a policy proposal. Not all assumptions are listed; rather, the key assumptions are those assumptions which are likely to have the greatest impact on the costing outcome and/or those which are the most uncertain.

4.2.3 Uncertainty

The PBO includes information on the factors affecting the reliability of a costing in our costing minutes. This is designed to highlight the level of confidence that a user of the costing can have that the actual impact of the policy costed would correspond to the costing estimate. Despite being our best possible estimates of the financial impact of a policy, all costing estimates are subject to some degree of uncertainty about how closely they would correspond to actual outcomes, were the proposal to be implemented.

The level of uncertainty will vary from costing to costing depending upon factors such as the:

- quality of the data available to undertake the costing

- number and soundness of any assumptions made in the costing analysis

- volatility of the costing base

- magnitude of the policy change.

We include information on factors that can materially affect uncertainty in all costings, highlighting particularly uncertain elements and providing information on the nature and extent of these elements.

For further details, see Factors influencing the reliability of policy proposal costings.

4.3 Modelling

The modelling approach used to generate a costing estimate varies considerably from one proposal to the next. It depends on the policy specification, the available data and assumptions, and involves building a model that draws upon these elements to estimate both the baseline and policy simulation impacts on the Budget. The approaches taken to estimating the impact of interactions between policy proposals and decisions around rounding are other important elements of the methodology.

A description of the methodology used to estimate the policy costing is provided in the costing minute, including details of the type of model used and the general processes followed in order to produce the costing estimates.

4.3.1 The modelling framework

Bottom-up versus top-down models

Costing models come in a number of forms. Some are bottom-up models which draw upon detailed individual unit record data for affected individuals. Some are top-down models that take aggregate data and determine the proportion of payments or receipts that would be affected by the policy change. And, of course, there is a spectrum of approaches in between involving a variety of levels of detail and combinations of approaches.

The modelling methodology that we choose for any particular costing will depend on the specifics of the policy proposal, the data that is available, the models that are available and the time available to complete the costing. Ultimately the choice of method will aim to produce the best estimate of the fiscal impact of the proposed policy given the available time and resources. The approach taken to building a model will have a bearing on the level of detail of the results that can be produced and on the time taken to construct the model and provide results.

Bottom-up approaches use detailed information on large numbers of individuals to build a model to analyse the policy. This approach often involves building a microsimulation model, which uses detailed unit record (or ‘micro-level’) data to simulate the effects of the policy proposal. The ‘records’ concerned are usually based on government administrative data which provides details of the characteristics of the individual transactors (but not their identity) and the value of the transactions concerned. This can include records of transactions by individual taxpayers or individual recipients of government payments. For instance, Social Security family benefits administrative data are ideal for estimating the cost of a change in Family Tax Benefit payment rates and provide detailed information on the households affected by a change.

The key advantage of a bottom-up approach is the level of detail it provides and hence the ability to undertake distributional analysis of a proposal. On the other hand, however, this approach is highly resource intensive and the results are highly dependent on the quality of the micro-level data and behavioural assumptions that underpin the analysis.

A top-down approach is much less resource intensive as it does not require unit record level detail or rely on the use of complex microsimulation models. It works well in cases where aggregate relationships are relatively stable, where detailed data is not available or where the costing must be completed quickly. For instance, a proposal to pay a back-to-school allowance for each child in a family that is in receipt of Family Tax Benefit Part A could be estimated by simply taking the aggregate number of children in these families multiplied by the proposed payment. Under this approach, aggregate level data, such as the total value of transactions and the average payment or tax rates, are used to derive the total value of payments or receipts.

The main disadvantage of a top-down approach is that it does not provide distributional information such as who is affected by a proposal. In the above example, the top down costing approach to the back-to-school allowance would provide an accurate costing estimate, but would not provide information about the characteristics of the families who would benefit from the proposal.

4.3.2 Baseline and simulation estimates

The costing model that is developed for a particular policy proposal is used to estimate the budget outcomes under both the baseline and policy simulation scenarios. The difference between these two estimates for each financial year of the costing period represents the cost of the policy proposal:

Costing(t) = SIMULATION(t) - BASELINE(t)

Where t is the relevant financial year.

Most costing models are ‘partial models’ of the Budget. They focus on just those parts of the Budget that are affected by a particular policy proposal and assume that all of the other transactions in the Budget remain unchanged.

Baseline estimates

The baseline estimates used in the costing process can be estimated in a number of ways:

- for a proposal that would introduce a completely new expenditure or revenue, the baseline forward estimates values would be zero

- for a proposal that modifies an existing expenditure program or revenue stream for which estimates are provided in the Budget, the estimates that are included in the most recent Budget update will be the baseline

- for a proposal that modifies an existing expenditure or revenue program for which estimates are not separately identified in the Budget, for instance because the modifications occur at a level of detail not provided in the budget estimates, we estimate the relevant baseline values based on the current forward estimates policy parameters

- In situations where the costing request seeks a disaggregated distributional analysis of the results, the PBO also needs to estimate a disaggregated set of baseline estimates.

Simulation estimates and adjusting for behavioural changes

The policy simulation involves changing the model from its baseline settings to incorporate the new policy specification. These changes may involve changing existing model parameters or making structural modifications to the model, for instance to add new entitlements, extend target populations or change means-testing arrangements.

An important component of any policy simulation involves an assessment of the likely direct behavioural changes that are expected to have a material impact on the costing result. These effects are incorporated in the model, either through adjustments to the built-in model parameters or by changing the structure of the model.

Not all policy proposals will result in a significant behavioural response. For costings that do not impact on market prices, where the transactions concerned are not price sensitive or where take-up rates are not an issue, behavioural responses would not be expected to be significant.

In many cases, however, policymakers change policy settings precisely in order to induce certain behavioural and economic changes. These effects become important where a proposal is likely to impact on price sensitive transactions or where they depend significantly on take-up rates. A proposal may affect how much people work, the quantities and types of goods and services that are consumed, and the amount that people save. For example:

- an increase in the excise on beer would be expected to increase the price of beer, which is likely to reduce beer consumption and increase consumption of substitute products like wine and spirits

- an increase in child care payments will effectively reduce the cost of child care and increase the demand for or supply of child care places, increasing the number of places that are subsidised.

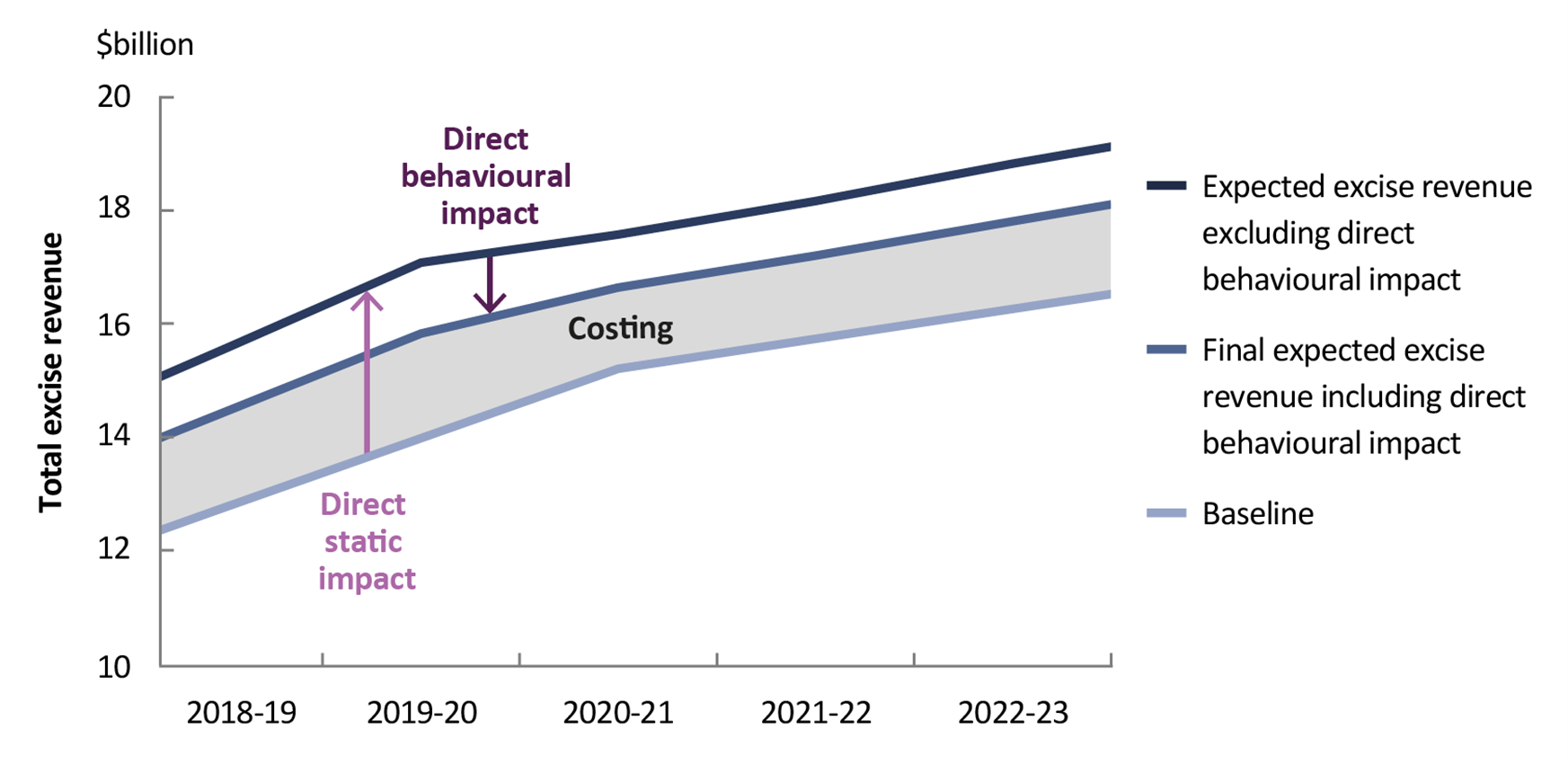

Box 2: Increase in tobacco excise—a straightforward policy costing.

|

A simple example of a policy proposal to increase the rate of excise duty applied to tobacco by 15 per cent from 1 September 2018. The steps in calculating the impact of this proposal are:

Excise duty is applied to tobacco before GST is applied, therefore increasing te excise on tobacco would also increase the amount of GST paid on tobacco products. As the net GST impact after forwarding additional revenue to the states and territories would be expected to be small, this is not reflected in the graph. Costing example - increase in the tobacco excise rate

|

Interactions between policy proposals

An interaction effect may need to be taken into account where a costing has multiple revenue or expense items, has a number of components with overlapping policy implications, or is part of a package of policy proposals that are proposed to be implemented together.

For example, consider a package of measures that included the payment of a $1,000 taxable grant to small businesses to purchase office productivity equipment and a reduction in the small business company tax rate from 30 per cent to 28 per cent. For a small business that has taxable income of $100,000, each measure in isolation would have the following impact on the Budget:

- the taxable grant would have a cost of $1,000, offset by tax payable on the grant of $300 giving a net cost of the grant of $700

- the reduction in the company tax rate would cost $2,000 (this figure only includes the direct static impact relating to the change in the tax rate).

The sum of the two components in isolation would be $2,700. Taken together, the impact of the two measures is a cost of $2,720. The extra $20 cost is an interaction effect that arises because the reduction in the small business company tax rate reduces the tax payable on the taxable grant, increasing the net cost of the grant (ie the $300 becomes $280).

Interactions may be complementary or compounding in their effects, or they may act as substitutes and lessen the overall impact of a costing. Note that the order in which interacting components are costed can change the costing estimates attributed to individual components of a package of measures, however the combined cost of the interacting components does not depend on their order. The PBO considers interaction effects in all costings.

Projections outside modelled timeframes

Costings are generally presented over a ten year period. In some cases, longer periods may be examined, particularly for policies where it is important to take account of long-term implications.

Where estimates need to be generated for periods outside those captured in the costing model, they need to be projected using representative growth rates. These growth rates will:

- be as representative as possible of growth rates for the data concerned

- be as consistent as possible with growth rates used for the forward estimates more generally

- represent the growth in the nominal value of the transaction base.

In practice, the PBO bases these growth rates on the economic parameters from the most recent Economic and Fiscal Outlook for the forward estimates period and will use the parameters underlying our ten year projections for longer time periods.

4.4 Quality assurance

Quality assurance is a critical aspect of the costing process. The PBO’s approach to costing policy proposals includes quality assurance across the four steps of the costing process outlined above. Elements of quality assurance include:

- consultation with Government agencies on the development of common costing models, assumptions and approaches

- internal peer review and senior executive clearance of each response to a costing request

- ex-post analyses of completed costing responses, including consultation with relevant external experts where possible.

Our ongoing work program involves continuously improving the costing models, data and approaches that are used to assess the fiscal cost of policy proposals. Consultations with agencies and experts external to Government are done in a manner that, where required, maintains the confidentiality of any related costing request.

4.5 Matters of presentation

A range of other adjustments are made to model-based costing estimates. The most important of these are:

- adjustments to reflect how a policy affects different budget balances

- assessments of the impact of the proposal on the interest payments that Government makes on public debt

- rounding adjustments that reflect the precision of costing estimates

- the treatment of costing estimates that are ‘unquantifiable’.

4.5.1 Budget balances

In the Australian Government Budget, there are three different measures of the budget balance that are published and referred to. These are: the fiscal balance, the underlying cash balance and the headline cash balance. The differences between the budget accounting treatments of these three measures are presented in Table 1.

In the Budget, the financial impact of all new policy proposals are generally only provided as ‘accrual’ estimates which show the impact on the fiscal balance. In PBO costings, we present the impact on the fiscal balance in the first instance, and report the financial implications on an underlying cash balance basis where these differ.

Differences between the fiscal and underlying cash balance impacts most commonly arise due to there being a timing gap between when the events that give rise to a payment occur and when cash payments are actually made. For instance, the obligation for the Government to make some payments to individuals may accrue over the course of a year, but the cash payment may not be made until a claim is lodged for payment by the payee in the next year.

The PBO also reports the financial implications of proposals on a headline cash balance in the case of proposals that involve transactions in financial assets which would otherwise not be reflected in a fiscal balance or underlying cash balance measure. Similarly, where we determine it to be warranted, the impact on other aspects of the Budget, such as net worth, will be reported.

Table 1: Different measures of the budget balance

| Reporting benchmark | Definition |

|---|---|

| Fiscal balance | This measures the change in the net worth of the Australian Government and is based on accrual accounting standards. This approach measures the value of transactions that give rise to an account being receivable the the Australian Government as arising when those transactions occur rather than when cash payment is made. The calculation of the fiscal balance is based on international standards. |

| Underlying cash balance | This measures the budget outcome in terms of the Australian Government's cash flow position, excluding transactions in the financial assets and future fund cash earnings. Transactions are measured at the time cash revenues are received or when cash payments are made. |

| Headline cash balance | This measures the budget outcome in terms of the change in the Australian Government's holding of cash assets. It includes transactions in financial assets and future fund cash earnings. Transactions are measured at the time cash revenues are received or when cash payments are made. |

4.5.2 Treatment of public debt interest payments

All Budgets contain estimates of the interest payments expected to be made by the Australian Government on the outstanding stock of public debt―these are called the ‘public debt interest’ (PDI) expenses.

All policy proposals that alter the Budget will have a PDI impact, however in most cases the PDI impact is sufficiently small that we do not include this in the individual costing estimates. The aggregate PDI impact of all new policy measures is included in our Post Election Report which captures the full policy platform for each designated parliamentary party.

An exception is made, however, where policy proposals involve the transactions in financial assets. In these cases, the PDI impact is included in the individual costing.

Factors taken into consideration when deciding to explicitly take account of PDI impacts in costings include:

- Does the proposal have a clear policy link to the level of interest payments that beneficiaries of the policy will pay

- In particular, does the policy/analysis relate to the transaction of financial assets (for example loan schemes, equity injections)?

- Is the PDI impact significant?

- In particular, if the impact on PDI payments was not included, would the aggregate impact of the proposal (fiscal balance, underlying cash balance or headline cash balance) present a misleading indication of the impact of the proposal on the Budget?

4.5.3 Rounding

In presenting costing estimates, the PBO is aware that there are errors in estimation, which will generally increase in proportion with the size of an estimate and the uncertainty of the source data and assumptions used to produce an estimate. The purpose of rounding estimates is to retain the meaningful information within an estimate while discarding spurious information.

The more uncertain an estimate is, the larger the rounding factor applied will be relative to the costing estimate. The methodology section of our costing minutes includes information on the rounding that has been applied when reporting the costing estimates.

4.5.4 Unquantifiable estimates

Where a proposal cannot be reliably costed, the financial implications will be reported as unquantifiable. The financial impact of a proposal that is reported as unquantifiable is not zero, and may be very substantial. Accordingly, unquantifiable costings are avoided wherever possible because they do not provide useful information for input into decision making and may provide a misleading picture of the financial impact of a proposal.

The main reason why a costing is unquantifiable will be a lack of reliable data or a very high level of volatility in the data used to cost the proposal. Lack of data may be overcome to some degree by making assumptions about the values of missing variables to derive the order of magnitude of the cost of a particular proposal, although this will increase the uncertainty of the estimates. Volatile data is more difficult as volatility is an indication that it may not be possible to reliably cost a proposal.

Wherever possible we avoid unquantifiable estimates, and provide at least an indication of the expected order of magnitude of a costing.

5 The costing minute

The costing minute is the document provided in response to the request of a parliamentarian or appearing in our Post-Election Report. It generally includes all of the key outputs from the costing process.

This includes:

- A summary of the policy proposal.

- Estimates of the impact of the implementation of the policy proposal on each of the different budget aggregates (fiscal balance, underlying cash balance and headline cash balance) over the forward estimates (the current budget year plus the three following years).

- Detailed estimates of the budget impact over the medium term (generally ten years, although longer if we deem this is warranted) including:

- Disaggregated estimates, where possible, by individual expenditure, revenue and net capital investment line items.

- Disaggregated estimates across the discrete elements of a policy proposal, where relevant.

- Estimates of the change in departmental resources required to implement the policy proposal (the minute provides a rationale where departmental costs of administering the policy are not included).

- A summary of the methodology and assumptions used to generate the costing.

- Identification of the data sources that underpin the costing.

- A statement about the factors affecting the reliability of the costing estimates.

- Additional analysis, if requested.

Examples of costing minutes

Examples of costing minutes are available in the PBO Election Commitments Reports. They show the layout of some typical PBO costings and how various elements of the costing are set out.

2016 PER ALP026—Not proceeding with income tax cuts for high-income Australians

This costing provides a good example of a policy proposal that has financial implications where there is a significant difference between the financial implications within and beyond the forward estimates period. It includes behavioural response assumptions and the methodology section sets out the separate calculations required for the costing.

2016 PER GRN033—Universities: Base Funding Lift

This costing is a good example of a costing that reports impacts on each of the fiscal balance, underlying cash balance and the headline cash balance and, because it involves student loans, includes an estimate of the impact of the proposal on public debt interest.