Policy costings are inherently uncertain – they may change over time, often by quite significant amounts. This Budget Bite explains why costings with the same policy specification can change as a result of revised economic forecasts, or using different time periods.

Costing estimates can be reported over different periods

A costing is an estimate of how a policy change (what the Budget papers call a ‘measure’) will affect the budget in the future. It represents the difference between the financial impact of an existing policy – for instance, the amount of revenue raised by a particular tax, or the cost of a program – and the financial impact of the new policy. Costings take into account economic forecasts, which will change over time.

New government measures are usually reported over the ‘forward estimates’ period – that is, the budget year and the following 3 years (4 years in total). Sometimes the impact may be announced for a longer period, such as the ‘medium term’, which includes 7 additional years past the forward estimates period (11 years in total).

For example, the government may announce a new policy which is expected to cost $20 million each year. This may be referred to as costing ‘$80 million over the forward estimates’ ($20 million by 4 years). Alternatively, the policy could be announced as costing $220 million over the medium term ($20 million by 11 years). This is the same policy and the same annual cost, just added up over a different time frame.

The ‘forward estimates’ period may not be enough to understand some costings

The most appropriate costing period depends on the nature of the policy. The impact of some policies may not be fully realised for several years, sometimes until after the end of the 4-year forward estimates. This may be due to lags in the collection of taxation receipts, or the time taken to set up and implement certain programs.

As an illustration, the 2023-24 Budget measure Better targeted superannuation concessions is estimated to increase tax receipts by $950 million over the forward estimates (see Figure 1). The description of the costing in the budget states that the measure will raise $2.3 billion in 2027-28. This is the first year outside the forward estimates period and the total is significantly more than the final year of the forward estimates. In cases like this, looking solely at the forward estimates period does not fully capture the ongoing impact of a policy.

Figure 1: Budget measures generally only provide information over the forward estimates period

Changing the reporting time period changes the value of the costing

Because budgets are put together on a rolling basis, at each annual budget the years covered by the forward estimates and medium-term change. Specifically, the first estimates year from the previous budget becomes an ‘actual’, and a new year is added to both the forward estimates and the medium term. For instance, the 2022‑23 Budget medium term covers the years 2022‑23 to 2032‑33, while the 2023‑24 Budget medium term covers 2023‑24 to 2033‑34. Different policies costed over the same time period are generally comparable, but 2 costings of the same policy conducted over different periods cannot be compared in the same way.

Although governments occasionally choose to provide an update, budgets do not routinely present new estimates of costings for policies announced in previous budgets. Where a policy costing is updated, the new estimates will usually cover a different time frame, potentially making a comparison confusing.

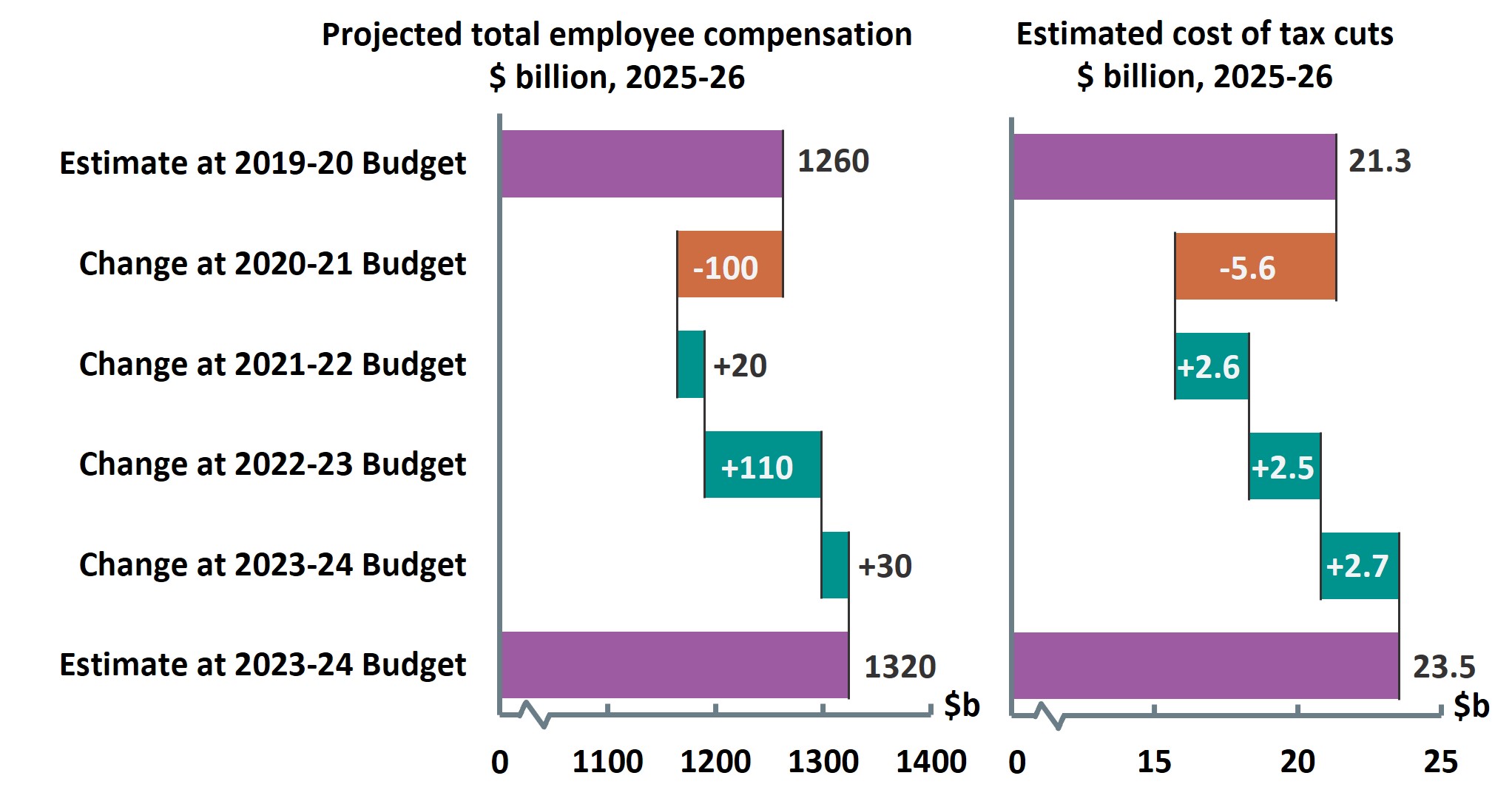

An example is the costing for the ‘Stage 3’ tax cuts. This policy was announced in the 2019-20 Budget, and various figures for the cost of the policy have been published since then.1 Figure 2 shows how the PBO’s estimates of the policy’s medium-term cost have changed since it was announced. Nearly all the changes reflect 2 factors – additional years being added to the medium-term period and the economic assumptions.

The Stage 3 tax cuts were to be implemented from 2024-25, beyond the then ‘forward estimates’ period for the 2019-20 Budget. A PBO costing of this policy estimated the total cost to be $145 billion over the medium term, which at that time ended in 2029-30 (6 years after the policy begins). The cost in that final year was $29.5 billion.

Now using the 2023-24 Budget as the starting point, the medium-term extends to 2033‑34. The total estimated cost over the medium term is $313 billion, which covers 10 years rather than 6 years. The cost in 2029-30 is $32.0 billion, around 8% higher than at the 2019‑20 Budget, with the difference mainly reflecting the revised budget assumptions about wages and employment.

Figure 2: Each Budget adds an additional year to the medium-term estimates of the Stage 3 tax cuts

Changes in the economy affect the cost of a policy

The outlook for the Australian economy changes over time. In recent years, the pandemic and then unexpected higher inflation greatly affected economic projections published at budget updates.

When economic projections change to reflect new economic data or the new context, the estimated costs of policies change too. For example, the inflation rate affects payments linked to the consumer price index, as well as how quickly wages are likely to grow, which in turn affects income tax collections.

Figure 3 shows that revisions over recent budgets to the estimated cost of the Stage 3 tax cuts in 2025-26 closely followed revisions to projections for compensation of employees (the total amount of wages and salaries paid to workers). Due to bracket creep, higher wages mean income earners pay higher rates of tax, magnifying the impact of income tax changes. Wages are the largest component of income, but the relationship is not one-to-one because non‑wage income, such as business and interest income, also affects the estimated cost of the tax cuts.

Figure 3: Changes in the estimated cost of Stage 3 tax cuts follow changes in economic projections

The PBO’s Build your own budget tool may be used to examine how changes to economic projections affect some policy changes. Table 1 shows the indicative impact of higher or lower inflation across different policy costings. Higher inflation increases the impact of a policy, with some policies sensitive to even small changes.

Table 1: Changes in economic parameters affect costing values

|

Fiscal balance impact of proposal ($b in 2033-34) |

|||

|---|---|---|---|

| Policy |

Baseline |

Inflation 1ppt higher |

Inflation 1ppt lower |

| Raise Jobseeker by $40 per fortnight |

-1.04 |

-1.15 (+10.6%) |

-0.94 (-9.7%) |

| Lower Fuel Excise by 10c per litre |

-8.01 |

-8.83 (+10.2%) |

-7.27 (-9.3%) |

| Remove 6.5% cap on public hospital funding growth |

-2.95 |

-4.04 (+37.3%) |

-2.06 (-30.3%) |

| Increase the tax-free income threshold to $20,000 |

-5.90 |

-5.97 (+1.2%) |

-5.82 (-1.4%) |

| Index the Age Pension to CPI |

2.10 |

2.41 (+14.7%) |

1.75 (-16.7%) |

Source: 2023-24 Budget and PBO analysis. Note: Inflation scenarios are assumed to impact both the consumer price index and the wage price index from 2023-24 to 2033-34. Other economic projections are as at the 2023-24 Budget.

Different data and methodologies produce differing costing results

Data and assumptions underpinning costings can also change over time or between different costings tools. And policy costings, whether undertaken by the PBO or by government more generally, make use of different models for different types of analysis.

The choice of model used can produce different financial estimates, although these differences are often more at the margin than the differences that arise from adding years or varying economic assumptions. For example, the Build your own budget tool can be used to explore scenarios for the personal income tax system based on aggregate tax data. The tool estimates that the Stage 3 tax cuts will cost around $320 billion over the medium term. However, for formal costing requests on stand-alone policies, the PBO may also use more detailed unit record tax-return data, which estimates a Stage 3 cost of $313 billion (around 2% lower). While both model estimates are of a similar magnitude, given the size of the program, they are constructed to service different purposes and the different results reflect those purposes.

Finally, costings sometimes involve technical assumptions, particularly regarding how affected individuals or businesses may respond to the policy change. For example, a change in the rate of tobacco excise will change smoking rates. These behavioural effects also have margins of uncertainty, because the propensity of people to smoke itself reflects multiple variables, not just cost.

All costing agencies make judgements about what behavioural assumptions to make. When we decide what assumptions we will use for PBO costings we consider a range of sources, such as academic literature, historical analysis of similar policies and consistency with previous similar costings. This process is explained further in Understanding behavioural assumptions used in policy costings.

Presenting uncertainty in costings and forecasts

The 2 main sources of uncertainty in costings are uncertainty in future economic conditions and uncertainty in the response to the policy. All costings involve making assumptions about each. As new data becomes available, new evidence about behavioural effects comes to light, or as different models are developed to replace older ones, relevant judgements about those assumptions will inevitably change.

Costing estimates are often rounded to indicate uncertainty. However, 2 estimates that are close together may appear to be much further apart after rounding is applied (e.g. amounts of $549 and $551 may be rounded to $500 and $600 respectively). Similarly, rounding may obscure trends in costing estimates – for example, the unrounded cost of a policy may steadily increase, while the rounded cost may not.

Another way to present uncertainty is to provide a range of estimates, although this approach may not meet the perceived need for certainty. There is a statement on this theme attributed to the Texan rancher and US President Lyndon B. Johnson. He is supposed to have replied, when presented with estimates in a likely range of values: ‘Ranges are for cattle. Give me a number’.2

The normal preference of users for point estimates rather than ranges can best be seen in the budget context. In general, budgets are plans for the future, and budget documents communicate those plans. They are rarely, if ever, predictions of the future. Planning, unlike predicting, can be effective through credible forecasts, based on transparent assumptions and acknowledging the sources of risk and uncertainty.

The Charter of Budget Honesty Act (1998) governs the activities of both governments and the PBO. It requires that government budgets provide a ‘discussion of the sensitivity of those fiscal estimates to changes in those economic and other assumptions’. For the 2023-24 Budget, this is primarily provided in Statements 8 and 9 of Budget paper 1, which includes a series of ‘fan charts’ illustrating confidence intervals for key budget forecasts. The PBO’s Build your own budget tool can also explore the sensitivity of budget estimates to different assumptions. Both mechanisms help users understand uncertainty in budget forecasts.

- The Personal income tax plan was first announced in the 2018-19 Budget and included 3 stages of tax cuts. These tax cuts were extended further in the 2019-20 Budget.

- See, for example, Manski (2018), Communicating uncertainty in policy analysis.